Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The video below from Matthew Gardner, Windermere’s Chief Economist, refers to the effects of constricted inventory levels on the national housing market in a higher interest rate environment. Review the localized numbers that I gathered that pertain to King and Snohomish Counties and then check out what he has to say about the national trends.

Overall, inventory has been tight in 2023! Many people made moves in the pandemic-fueled market and are deciding to stay put. They utilized the lower interest rates to secure their long-term home and don’t see a need to move anytime soon. Did you know the average person stays in their home for 10 years?

Others are not completely satisfied with their homes but feel attached to the lower rate and are pushing through the discomfort until rates settle. Some are deciding to come to market because their homes do not fit their lives anymore and some are bucking the rates and getting creative with financing. The buyers working the creative financing route with rate buy-downs will be rewarded when rates lower and prices go up.

Year-to-date new listings in King County are down 30% over 2022 and down 37% in Snohomish County. Closed sales are down 27% over 2022 in King County and down 27% in Snohomish County. Even though there have been fewer new listings year-over-year, the closed sale percentage is tracking more favorably which demonstrates buyer demand. This is why inventory is tight. In August 2023 there were 1.3 months of inventory in King County and 1.1 months in Snohomish County. This illustrates a seller’s market.

Closed sales peaked in 2021 in both counties at 20,132 in King County and 8,663 in Snohomish County. As we venture away from these outlier pandemic years, consumers are wrapping their heads around the changing environment. Year-to-date, King County has had 16,069 closed sales and 5,344 in Snohomish County. Year-to-date, King County is pacing slightly higher than 2019, which was a normal market prior to the pandemic and Snohomish County is lagging behind by just a bit.

The pace of inventory has helped stabilize prices and created price growth since the start of 2023. Buyer demand exists because people’s lives change and we have the Millennial generation out in full force. If your life is leading you to consider a move, please reach out. Please do not rely on the noise in the media, they will lead you astray.

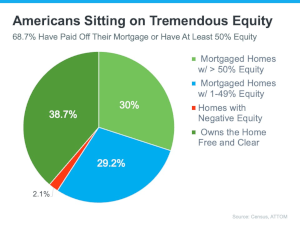

I can help you dig into the data and devise a plan that relates to YOUR life. With equity levels astoundingly high (over 50% of homeowners in the U.S. have over 50% equity), moves are being made with great success. For buyers, the rates can be overcome with some creativity, lived with for now, or you can set a benchmark for when you’re ready. If you are curious about how today’s market relates to your goals or want to make a plan for the future, let’s talk! It is always my goal to help keep my clients informed and empower strong decisions.

Were you like me and turned the heat on when the rain came this week? It’s that time of year when our heating systems need to be attended to, to be properly prepared for the colder months ahead.

Have your air and ventilation systems inspected by the professionals to ensure efficient and healthy airflow. This will also ensure that your systems are running safely and lower your risk of fire. Note: if you need to purchase or replace any major household appliances, September and October are usually when the latest models are revealed.

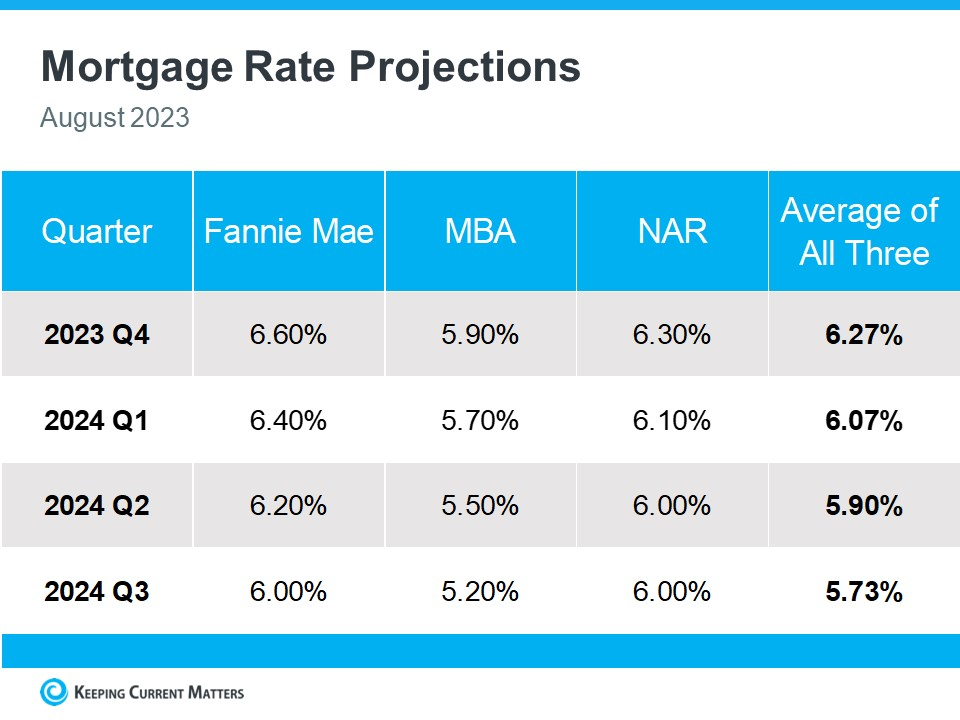

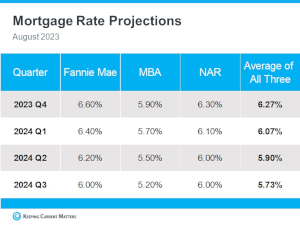

Most often a home buyer will procure a home loan with a 30-year term and the current interest rate. In the month of August, the 30-year conventional interest rate averaged 7.25%. While 7.25% is reflective of the average over the last 30 years, it is 2-3% higher than what we have experienced over the last 5 years. According to several experts, rates are predicted to decrease as we finish out 2023 and head into 2024. That also means that it is very likely prices will increase when that happens.

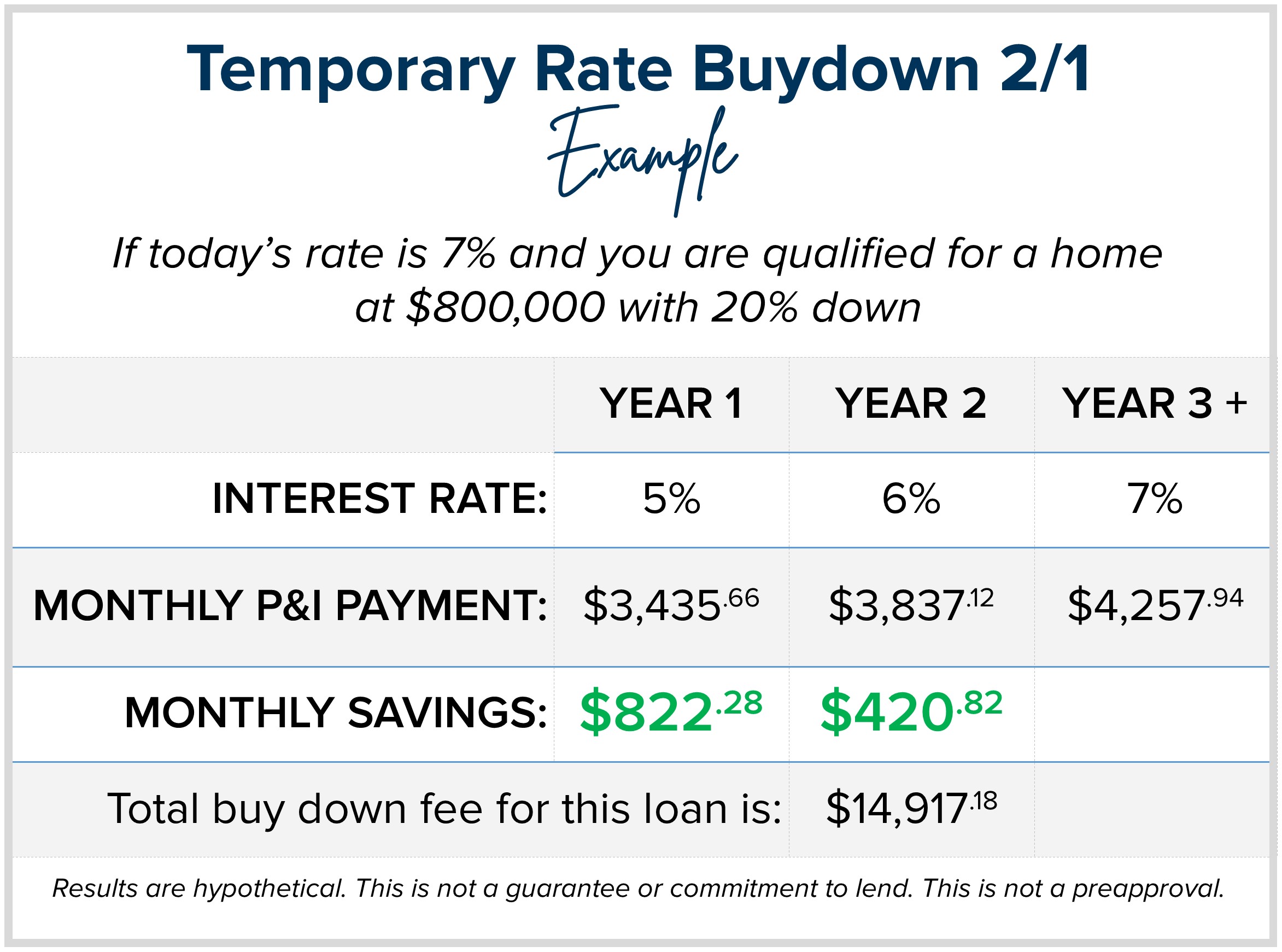

Most often a home buyer will procure a home loan with a 30-year term and the current interest rate. In the month of August, the 30-year conventional interest rate averaged 7.25%. While 7.25% is reflective of the average over the last 30 years, it is 2-3% higher than what we have experienced over the last 5 years. According to several experts, rates are predicted to decrease as we finish out 2023 and head into 2024. That also means that it is very likely prices will increase when that happens. Here is an example, let’s say you are shopping for a house and have the same $800,000 budget and a 20% down payment with today’s rate of 7%. The monthly principal and interest payment would be $4,257.94. You could do a 2-1 buydown (2 points lower in year one and 1 point lower in year 2) which would have your payment in year one be based on an interest rate of 5% with a monthly principal and interest payment of $3,435.66 – a savings of $822.28 a month. For year two, the monthly principal and interest would be based on 6%, resulting in a monthly payment of $3,837.12, a $420.82 savings. The total savings in monthly payments with the 2-1 buy-down over the two years would be $14,917.18.

Here is an example, let’s say you are shopping for a house and have the same $800,000 budget and a 20% down payment with today’s rate of 7%. The monthly principal and interest payment would be $4,257.94. You could do a 2-1 buydown (2 points lower in year one and 1 point lower in year 2) which would have your payment in year one be based on an interest rate of 5% with a monthly principal and interest payment of $3,435.66 – a savings of $822.28 a month. For year two, the monthly principal and interest would be based on 6%, resulting in a monthly payment of $3,837.12, a $420.82 savings. The total savings in monthly payments with the 2-1 buy-down over the two years would be $14,917.18.

Thank you to everyone who pitched in during the Summer Food Drive! Through your generosity, we collectively donated $3,060 and 1,503 pounds of food to Volunteers of America Western Washington food banks! This is all going directly into our communities to help our neighbors in need.

Thank you to everyone who pitched in during the Summer Food Drive! Through your generosity, we collectively donated $3,060 and 1,503 pounds of food to Volunteers of America Western Washington food banks! This is all going directly into our communities to help our neighbors in need.

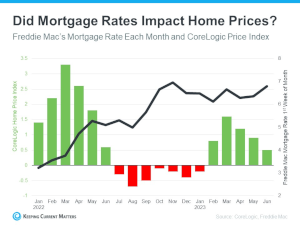

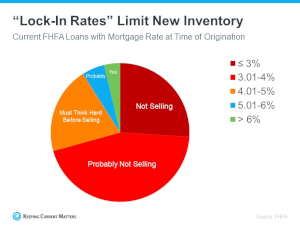

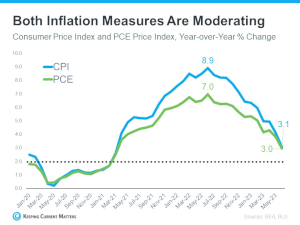

There has always been a direct correlation between interest rates and home prices. The rule of thumb has always been when rates go up prices go down, and vice versa. This was temporarily proven true in the summer of 2022 when rates quickly rose by 2% (3.5%-5.5%) over 5 months. It created a price correction in the second half of 2022 as buyers retreated from the market due to affordability. One should note that price acceleration was rapid from May 2020 to May 2022 and in that two-year period prices grew upward of 50% in King and Snohomish Counties. That was an unsustainable pace. In all honesty, this was inflation’s role in the housing market, and increasing the rates was the Fed’s way of getting control.

There has always been a direct correlation between interest rates and home prices. The rule of thumb has always been when rates go up prices go down, and vice versa. This was temporarily proven true in the summer of 2022 when rates quickly rose by 2% (3.5%-5.5%) over 5 months. It created a price correction in the second half of 2022 as buyers retreated from the market due to affordability. One should note that price acceleration was rapid from May 2020 to May 2022 and in that two-year period prices grew upward of 50% in King and Snohomish Counties. That was an unsustainable pace. In all honesty, this was inflation’s role in the housing market, and increasing the rates was the Fed’s way of getting control. Believe it or not, the higher rates are keeping prices stable because it is limiting the available inventory for sale. You see, there are plenty of buyers out looking for homes right now, and inventory levels are tight because potential sellers are waiting to make a move because they are holding on to their low rate. Our job market is good, we have people moving to our area and the millennials are out in full force searching for their first homes.

Believe it or not, the higher rates are keeping prices stable because it is limiting the available inventory for sale. You see, there are plenty of buyers out looking for homes right now, and inventory levels are tight because potential sellers are waiting to make a move because they are holding on to their low rate. Our job market is good, we have people moving to our area and the millennials are out in full force searching for their first homes. Here’s the deal though, housing is a reflection of life! According to the US Census, 66% of homeowners would like to upgrade to a nicer home with features that better match their lifestyle, and 45% would like to move to a home to better match the changing size of their household. Life changes motivate moves! Many people are waiting out these life changes until rates come down so they can better afford their desired transition. This has put downward pressure on inventory, limiting selection for buyers, hence creating price growth and stabilization.

Here’s the deal though, housing is a reflection of life! According to the US Census, 66% of homeowners would like to upgrade to a nicer home with features that better match their lifestyle, and 45% would like to move to a home to better match the changing size of their household. Life changes motivate moves! Many people are waiting out these life changes until rates come down so they can better afford their desired transition. This has put downward pressure on inventory, limiting selection for buyers, hence creating price growth and stabilization. We find ourselves in a delicate dance with inflation, rates, inventory, and prices. Someone who desires a move has to consider the impact the rates can have on their payment. Many of these buyers are taking the leap and finding creative ways to offset the rate such as ARM financing, rate buy downs, or they are preparing to re-finance their purchase when rates come down. This way they will have secured a good price which is the basis of their loan.

We find ourselves in a delicate dance with inflation, rates, inventory, and prices. Someone who desires a move has to consider the impact the rates can have on their payment. Many of these buyers are taking the leap and finding creative ways to offset the rate such as ARM financing, rate buy downs, or they are preparing to re-finance their purchase when rates come down. This way they will have secured a good price which is the basis of their loan.

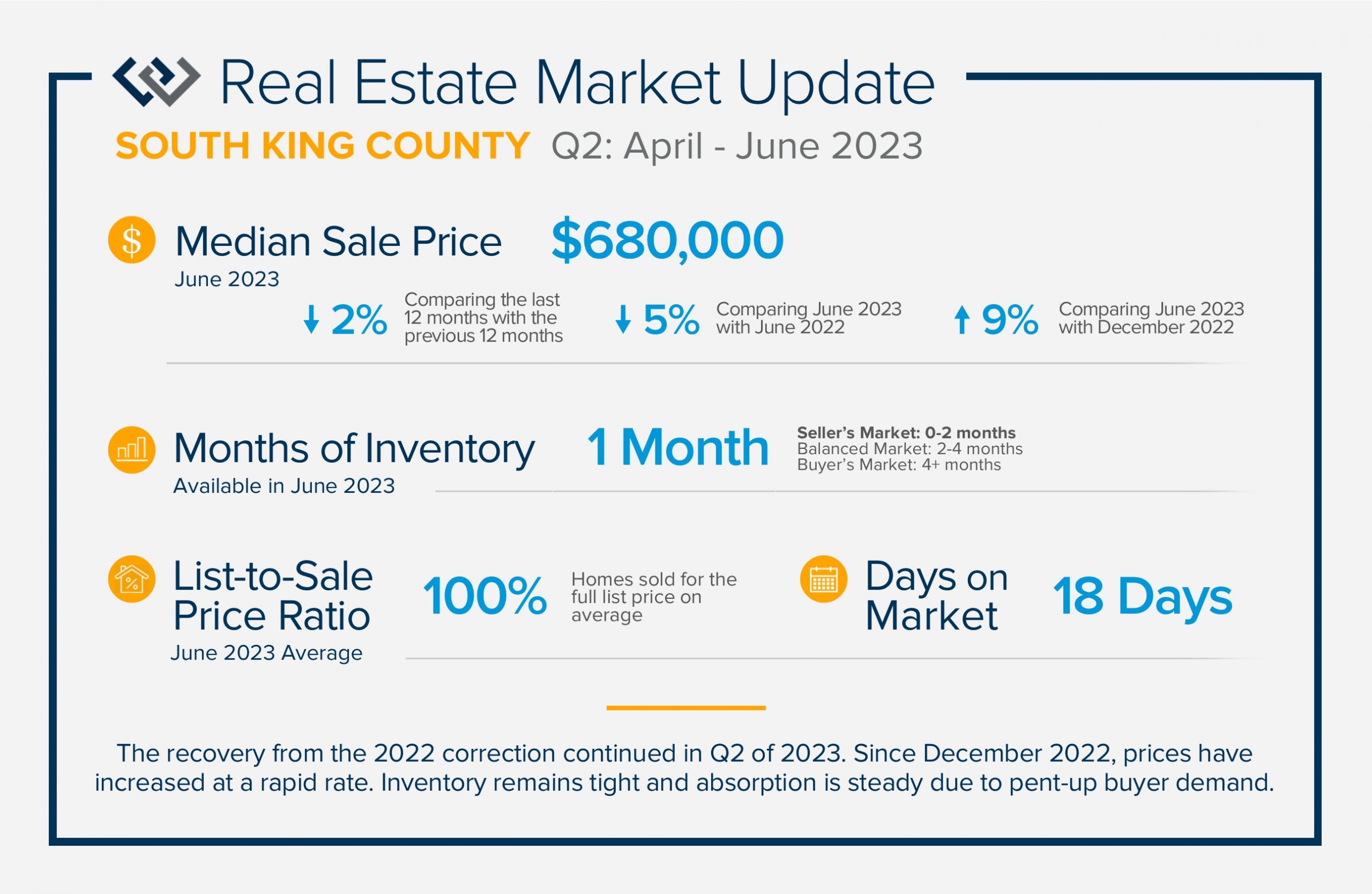

The recovery from the 2022 correction continued in Q2 of 2023. Since December 2022, prices have increased at a rapid rate. Inventory remains tight and absorption is steady due to pent-up buyer demand. Shorter days on market and healthy list-to-sale price ratios illustrate when a seller meets the market with appropriate pricing and is in good condition, a swift and successful sale is in store. Despite higher interest rates the market continues to churn. Rates are anticipated to come down, and when they do competition will increase.

The recovery from the 2022 correction continued in Q2 of 2023. Since December 2022, prices have increased at a rapid rate. Inventory remains tight and absorption is steady due to pent-up buyer demand. Shorter days on market and healthy list-to-sale price ratios illustrate when a seller meets the market with appropriate pricing and is in good condition, a swift and successful sale is in store. Despite higher interest rates the market continues to churn. Rates are anticipated to come down, and when they do competition will increase.

Windermere Community Service Day

Windermere Community Service Day

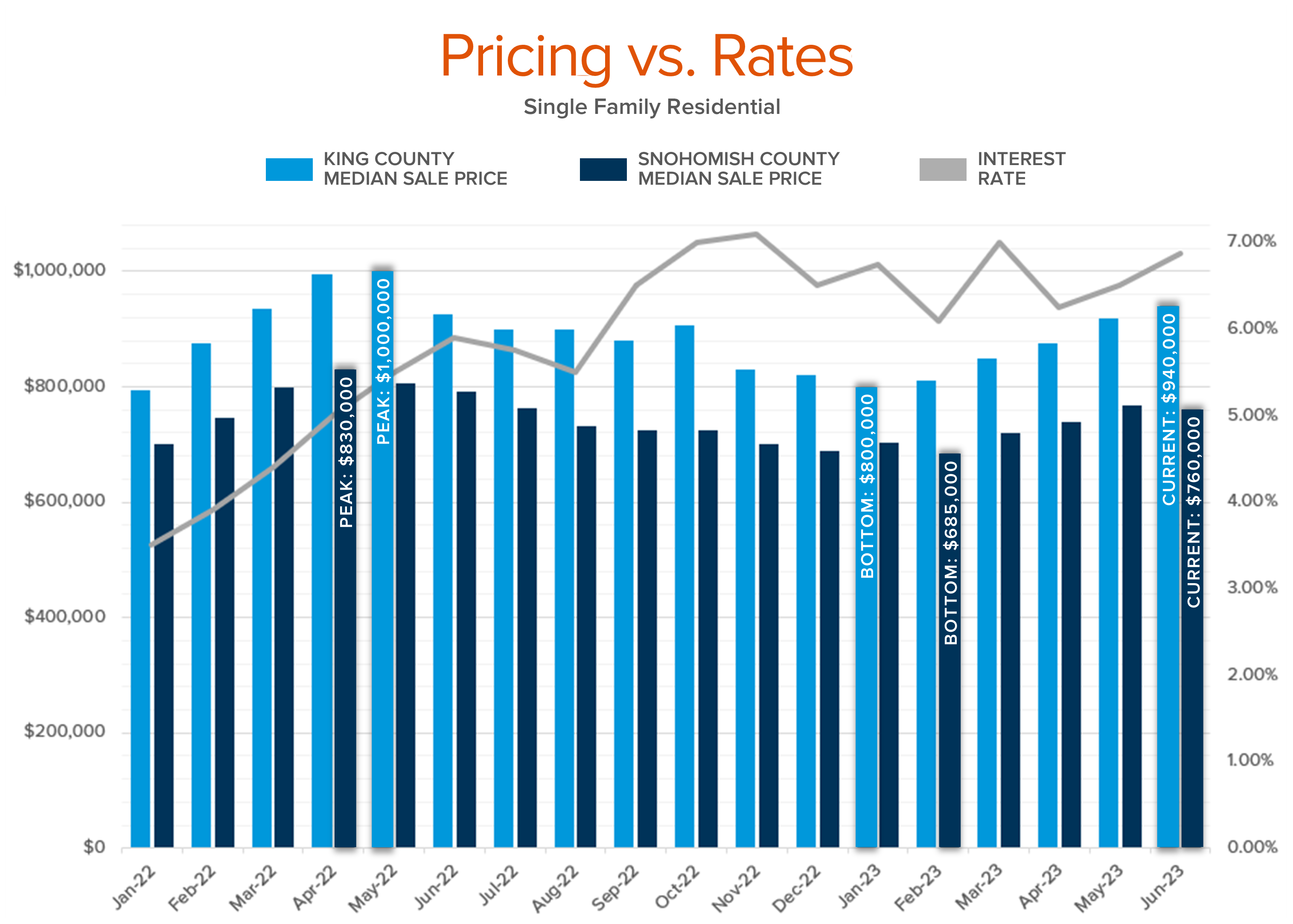

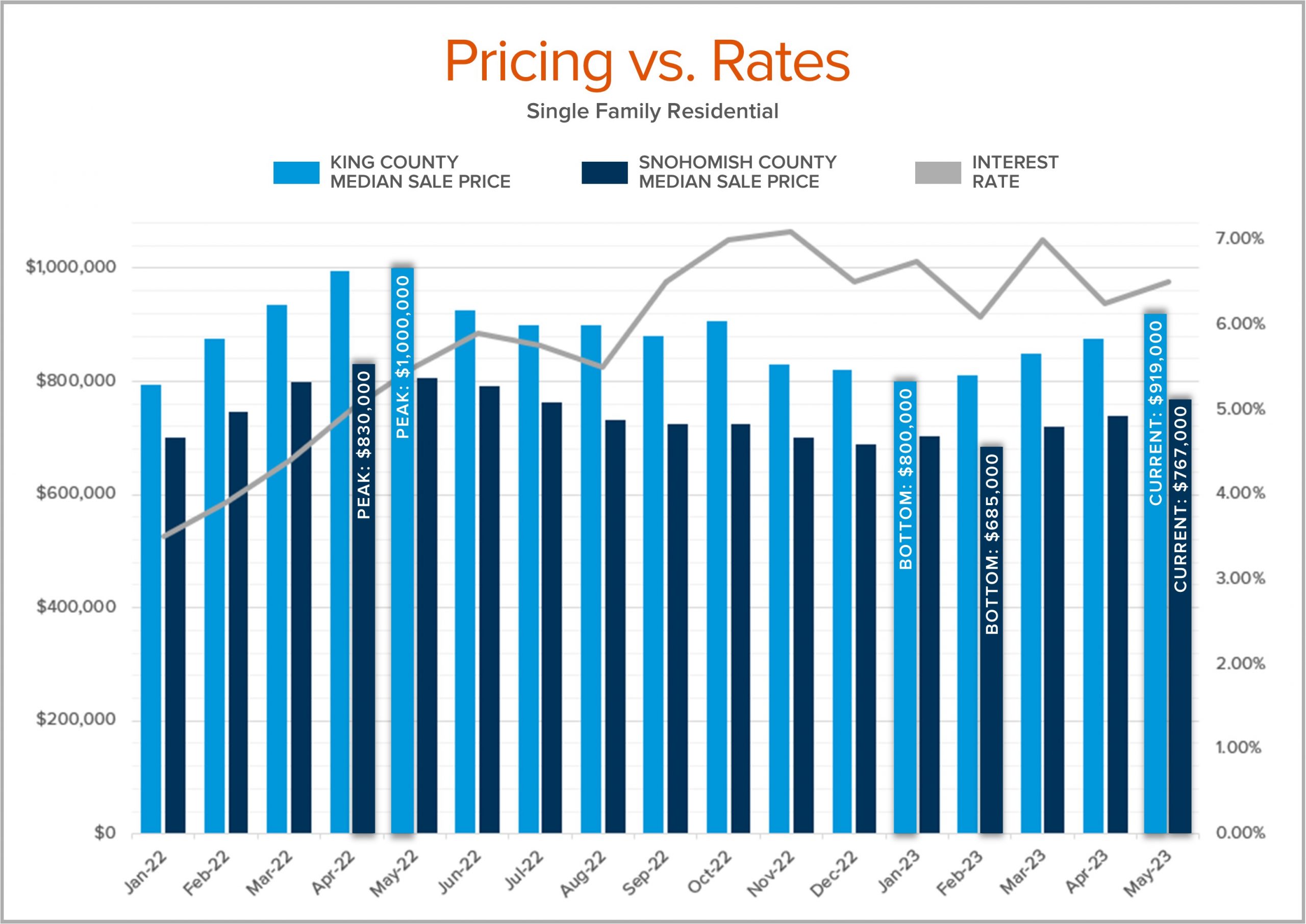

In King County, the median price peaked in May 2022 at $1M and is currently at $919,000 (May 2023), which is down 8% from peak to current. Prices hit bottom in January 2023 at $800,000 which was down 20% (the actual tumble) from the peak but are now up 15% from the bottom!

In King County, the median price peaked in May 2022 at $1M and is currently at $919,000 (May 2023), which is down 8% from peak to current. Prices hit bottom in January 2023 at $800,000 which was down 20% (the actual tumble) from the peak but are now up 15% from the bottom!

ATTENTION GARDENERS: Windermere Community Service Day is coming and we’d love your help!

ATTENTION GARDENERS: Windermere Community Service Day is coming and we’d love your help!

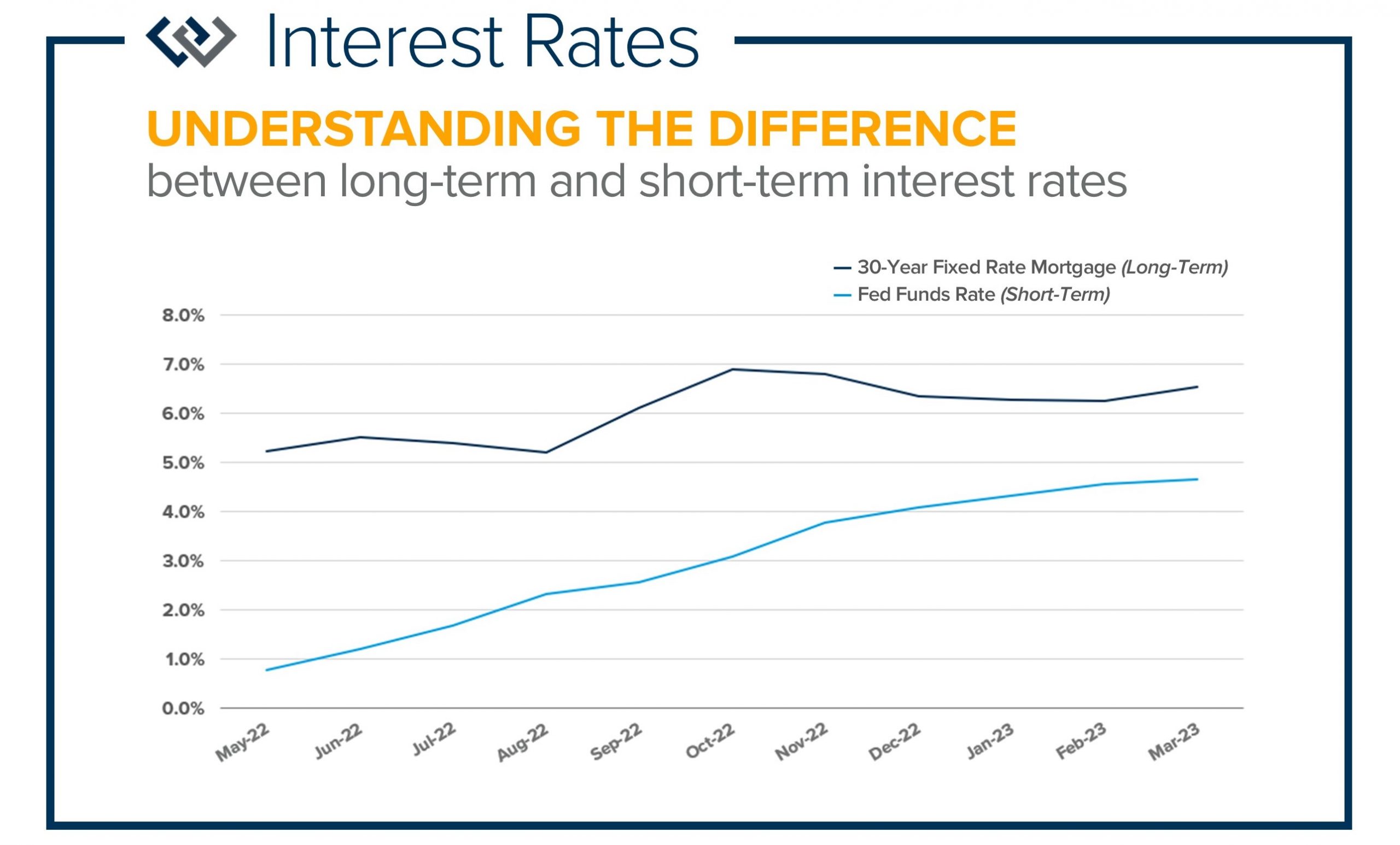

It is very important that consumers understand the difference between long-term interest rates and short-term interest rates. Long-term rates involve home mortgages such a conventional 30-year fixed, Jumbo, FHA, and VA loans. Short-term rates involve car loans, credit cards, and Home Equity Lines of Credit (HELOCs). While both types of rates have gone up over the course of the last year, they have not had the same trajectory.

It is very important that consumers understand the difference between long-term interest rates and short-term interest rates. Long-term rates involve home mortgages such a conventional 30-year fixed, Jumbo, FHA, and VA loans. Short-term rates involve car loans, credit cards, and Home Equity Lines of Credit (HELOCs). While both types of rates have gone up over the course of the last year, they have not had the same trajectory.

ATTENTION GARDENERS: Windermere Community Service Day is coming and we’d love your help!

ATTENTION GARDENERS: Windermere Community Service Day is coming and we’d love your help!

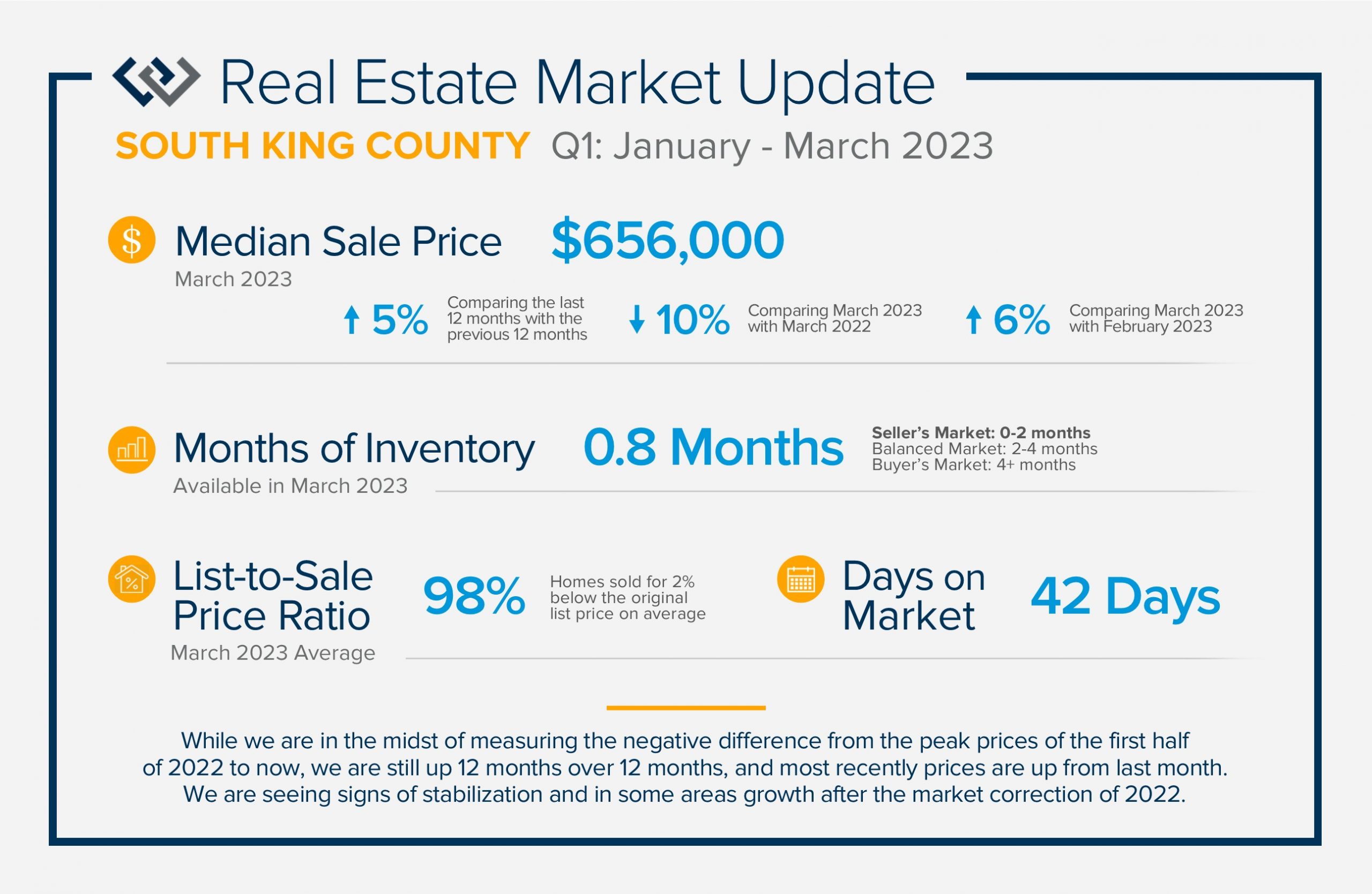

We are seeing signs of price stabilization and some growth after the market correction of 2022! Illustrated on the front is the up-down-up trajectory that home prices have experienced over the last year. While we are in the midst of measuring the negative difference from the peak prices of the first half of 2022 to now, we are still up 12 months over 12 months, and most recently prices are up from last month.

We are seeing signs of price stabilization and some growth after the market correction of 2022! Illustrated on the front is the up-down-up trajectory that home prices have experienced over the last year. While we are in the midst of measuring the negative difference from the peak prices of the first half of 2022 to now, we are still up 12 months over 12 months, and most recently prices are up from last month.